Dealing with a shattered windshield in Rock Hill, SC causes immediate frustration. Adding the confusing process of filing an insurance claim makes the situation much worse. Navigating automated phone systems, answering confusing coverage questions, and waiting for an adjuster creates massive delays. Professional insurance claim assistance removes this stress entirely. We guide you through the exact steps required to get your glass fixed fast. This guide details exactly how auto glass insurance claims work, what your policy actually covers, your legal rights in South Carolina, and how professional assistance prevents out-of-pocket surprises.

How Do Auto Glass Insurance Claims Work?

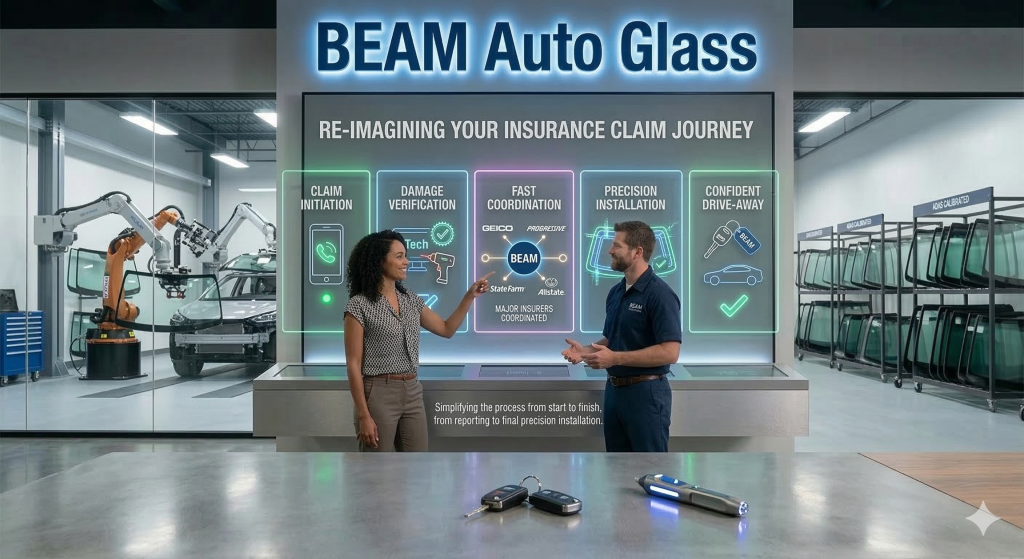

Filing a claim for broken glass follows a precise, predictable path when handled by experienced professionals.

Initial Damage Assessment

Technicians begin by inspecting the severity of the broken glass. They document the exact size and location of the impact point. This assessment determines if a simple resin injection fixes the problem safely or if a completely new pane of glass is required. Accurate documentation prevents the insurance adjuster from denying the necessary repair method.

Verifying Your Policy Coverage

Shop staff contact your insurance provider directly using dedicated merchant hotlines. They pull up your exact policy details to verify what repairs your plan pays for. This direct verification prevents you from receiving an unexpected bill after the repair is completed.

Filing the Claim Directly with the Provider

The auto glass shop submits the official repair request to the insurance company network. They provide all the necessary photographs, safety inspection reports, and repair estimates. This direct submission bypasses the slow customer service queues you would experience calling the provider yourself.

What Does Auto Glass Insurance Actually Cover?

Auto insurance policies divide coverage into several different categories. Glass damage usually falls under a very distinct section of your policy.

Non-Collision Coverage Explained

Most auto glass damage occurs without a vehicle crash. A stray rock kicked up by a commercial truck on I-77, a falling tree branch during a heavy thunderstorm, or severe hail all cause shattered glass. These incidents fall under “Other-Than-Collision” or full-coverage policies. If you carry this type of policy, your provider pays for the repair.

Windshield Chip and Crack Repair Coverage

Providers almost always pay for minor resin injections. Repairing a small chip stops the damage from spreading into a massive crack. Insurance companies prefer paying for a small repair now rather than paying for an expensive full replacement later.

Full Windshield and Window Replacements

When a crack spans longer than a few inches, or when a side window shatters completely, a new pane of glass is mandatory. Your full-coverage policy pays for the exact Original Equipment Manufacturer (OEM) equivalent glass, the specialized urethane adhesives, and the professional labor required to install the new window safely.

Advanced Safety Sensor Calibration Coverage

Modern vehicles require exact camera alignment after a windshield replacement. The forward-facing camera controls automatic emergency braking and lane-keeping assistance. Providers recognize this calibration as a mandatory safety requirement and cover the costs of resetting the sensors to factory standards.

How Does Professional Claim Assistance Prevent Delays?

Waiting days or weeks for an insurance approval leaves your vehicle vulnerable to further damage and water leaks. Professional assistance drastically reduces this waiting period.

Eliminating Confusing Paperwork

Filing a claim alone often requires navigating confusing online portals and uploading correctly formatted documents. Shop staff fill out the necessary digital forms accurately the very first time. They submit the exact photographic evidence the insurance adjuster requires to approve the claim immediately.

Direct Communication with Insurance Adjusters

Insurance adjusters sometimes push back on replacing a windshield, suggesting a repair instead. Technicians speak directly to the adjusters, explaining exactly why a repair compromises the structural integrity of the vehicle based on strict safety standards. This expert advocacy prevents the provider from dictating unsafe repair methods.

Faster Approval Times and Scheduling

Using established digital networks allows the shop to receive repair authorization rapidly. In many cases, the shop secures approval and schedules the actual physical work the very same day the damage occurs.

Do Auto Glass Claims Increase Your Monthly Premiums?

Many drivers hesitate to fix a broken windshield because they fear their monthly insurance bill will skyrocket.

“No-Fault” Damage Classifications

A rock hitting your windshield is considered an unpredictable, “no-fault” incident. You did nothing wrong to cause the damage. Insurance providers generally do not penalize drivers for filing claims related to weather, vandalism, or flying road debris.

The Difference Between Claim Types

Filing a claim because you rear-ended another car raises your rates because it indicates risky driving behavior. Filing a claim because a severe thunderstorm dropped hail on your vehicle falls under a completely different category. A single glass claim typically has zero impact on your insurance premiums.

Will You Have to Pay a Deductible in South Carolina?

A deductible is the initial amount of money you agree to pay out-of-pocket before your insurance covers the remaining balance. Auto glass deductibles operate differently depending on where you live.

South Carolina Zero-Deductible Auto Glass Laws

South Carolina law (SC Code Section 38-77-280) provides incredible protection for drivers. If your vehicle is registered in South Carolina and you carry full non-collision coverage, the law requires your insurance provider to waive your deductible entirely for safety glass repair or replacement.

Zero Out-of-Pocket Expenses

This exact state law guarantees you pay absolutely nothing out-of-pocket for a windshield replacement. Your insurance covers the entire bill. You do not need to pay a $500 or $1000 deductible first. The repair is completely covered.

What Qualifies as Safety Glass?

The zero-deductible law applies exactly to the windshield, side door windows, and the rear window. These pieces of glass are classified as structural safety components designed to protect occupants during a collision.

Can You Choose Your Own Auto Glass Shop?

Insurance providers sometimes attempt to direct you toward their own preferred network of auto glass shops. This practice often leaves drivers wondering if they have a choice in the matter.

Your Legal Right to Choose

Under South Carolina law, you possess the absolute legal right to choose exactly which auto glass shop repairs your vehicle. An insurance provider cannot force you to use a specific corporate chain or a substandard repair facility.

Avoiding “Steering” Tactics

Sometimes, third-party administrators working for the insurance company use a tactic called “steering” to pressure you into using their preferred network. They might suggest that using an independent local shop will delay your claim or void your warranty. Professional claim assistance experts from a local shop counter these tactics immediately. They handle the communication, protecting your legal right to receive high-quality, local service without intimidation.

What If You Only Carry Liability Auto Insurance?

The South Carolina zero-deductible law and general glass claim benefits rely entirely on the type of policy you purchase.

Understanding Liability-Only Limitations

Liability insurance only pays for the damage you cause to another driver’s vehicle during a crash. It provides absolutely zero coverage for physical damage to your own vehicle. If a rock strikes your windshield and you only carry a liability policy, you must pay for the repair out-of-pocket entirely.

Alternative Payment Options

If you lack glass coverage, reputable local auto glass shops provide exact, transparent pricing before any work begins. They offer competitive rates and explain exactly what the repair entails, allowing you to pay directly without hidden fees or surprise charges.

Why You Should Never Postpone Auto Glass Insurance Claims

Knowing that South Carolina waives the deductible means there is absolutely no valid reason to delay a repair. Postponing the claim creates severe risks.

Spreading Cracks and Worsening Damage

Changes in weather cause the glass to expand and contract. A tiny rock chip will inevitably split into a massive crack across your line of sight. A small, easily repairable chip quickly turns into a situation requiring a complete windshield replacement.

Failing State Safety Inspections and Traffic Tickets

Police officers actively issue traffic citations for vehicles operated with obstructed vision. A severely cracked windshield violates state safety laws. Addressing the damage promptly using your insurance coverage saves you from expensive tickets.

Risking Complete Windshield Failure

Your windshield provides up to 60 percent of the cabin’s structural strength during a rollover accident. A cracked windshield loses this strength. If you are involved in a collision, the weakened glass will shatter, allowing the vehicle roof to crush inward and the passenger airbags to deploy incorrectly.

Why Choose Local Rock Hill, SC Claim Assistance Experts?

Choosing a dedicated local shop in Rock Hill, SC, provides distinct advantages over calling a massive national call center.

Direct Billing Networks

Local experts possess established relationships with all major insurance agencies operating in the Upstate region. Once the shop files the claim and receives approval, they bill the insurance company directly. You never have to wait weeks for a reimbursement check to arrive in the mail.

Understanding Local South Carolina Insurance Policies

A national call center agent might not understand the specific nuances of South Carolina’s zero-deductible laws. Local Rock Hill technicians know exactly how to apply this state statute to your claim, guaranteeing you receive the completely free replacement you are legally entitled to under your full-coverage policy.

Guaranteed Workmanship

A local shop relies on a strong community reputation. They handle your insurance claim honestly and perform the physical repair using strict safety standards. You receive direct communication, exact appointment times, and a team that stands behind their labor.

Schedule Your Repair and Let Us Handle the Claim Today

Do not let confusing insurance procedures prevent you from fixing a dangerous, shattered windshield. Driving with compromised auto glass puts you and your passengers at severe physical risk. Our dedicated team handles the entire claims process directly with your provider, eliminating administrative headaches and long phone holds. We verify your exact coverage, enforce your legal right to a zero-deductible replacement under South Carolina law, and secure immediate repair authorization. We bill the provider directly so you never touch your wallet. Protect your family from failing safety sensors and weakened structural glass. Contact BEAM Auto Glass right now. We will file your claim, schedule your exact appointment time, and restore your vehicle safely to factory standards.